CYIENT LIMITED: “Nudging the culture”.

Date Published: September 18, 2023

Company Overview:

Cyient Limited (Cyient), formerly known as Infotech Enterprises Ltd, Cyient is a global Engineering and Technology Solutions company. We enable our customers to apply technology imaginatively across their value chain to solve problems that matter. Company is committed to designing tomorrow together with our stakeholders and being a culturally inclusive, socially responsible, and environmentally sustainable organization. Company is engaged in providing global technology services and solutions specialising in geospatial, engineering design, IT solutions and data analytics. Having its headquarters and development facilities in India, Company serves a global customer base through its subsidiaries in the United States of America (USA), United Kingdom (UK), Germany, Japan, Australia, Singapore and India. Cyient's range of services include digitisation of drawings and maps, photogrammetry, computer aided design/engineering (CAD/CAE), design and modelling, repair development engineering, reverse engineering application software development, software products development, consulting, analytics and implementation. Apart from these, it specializes in software services and solutions for the manufacturing, utilities, telecommunications, transportation & logistics, local government and financial services markets.

Industry overview:

The IT & BPM sector has become one of the most significant growth catalysts for the Indian economy, contributing significantly to the country’s GDP and public welfare. The IT industry accounted for 7.4% of India’s GDP in FY22, and it is expected to contribute 10% to India’s GDP by 2025. According to National Association of Software and Service Companies (Nasscom), the Indian IT industry’s revenue touched US$ 227 billion in FY22, a 15.5% YoY growth. According to Gartner estimates, IT spending in India is expected to increase to US$ 101.8 billion in 2022 from an estimated US$ 81.89 billion in 2021. Indian software product industry is expected to reach US$ 100 billion by 2025. Indian companies are focusing on investing internationally to expand their global footprint and enhance their global delivery Centre’s. The data annotation market in India is expected to reach US$ 7 billion by 2030 due to accelerated domestic demand for AI. In the Union Budget 2023-24, the allocation for IT and telecom sector stood at Rs. 97,579.05 crore (US$ 11.77 billion). The government introduced the STP Scheme, which is a 100% export-oriented scheme for the development and export of computer software, including export of professional services.

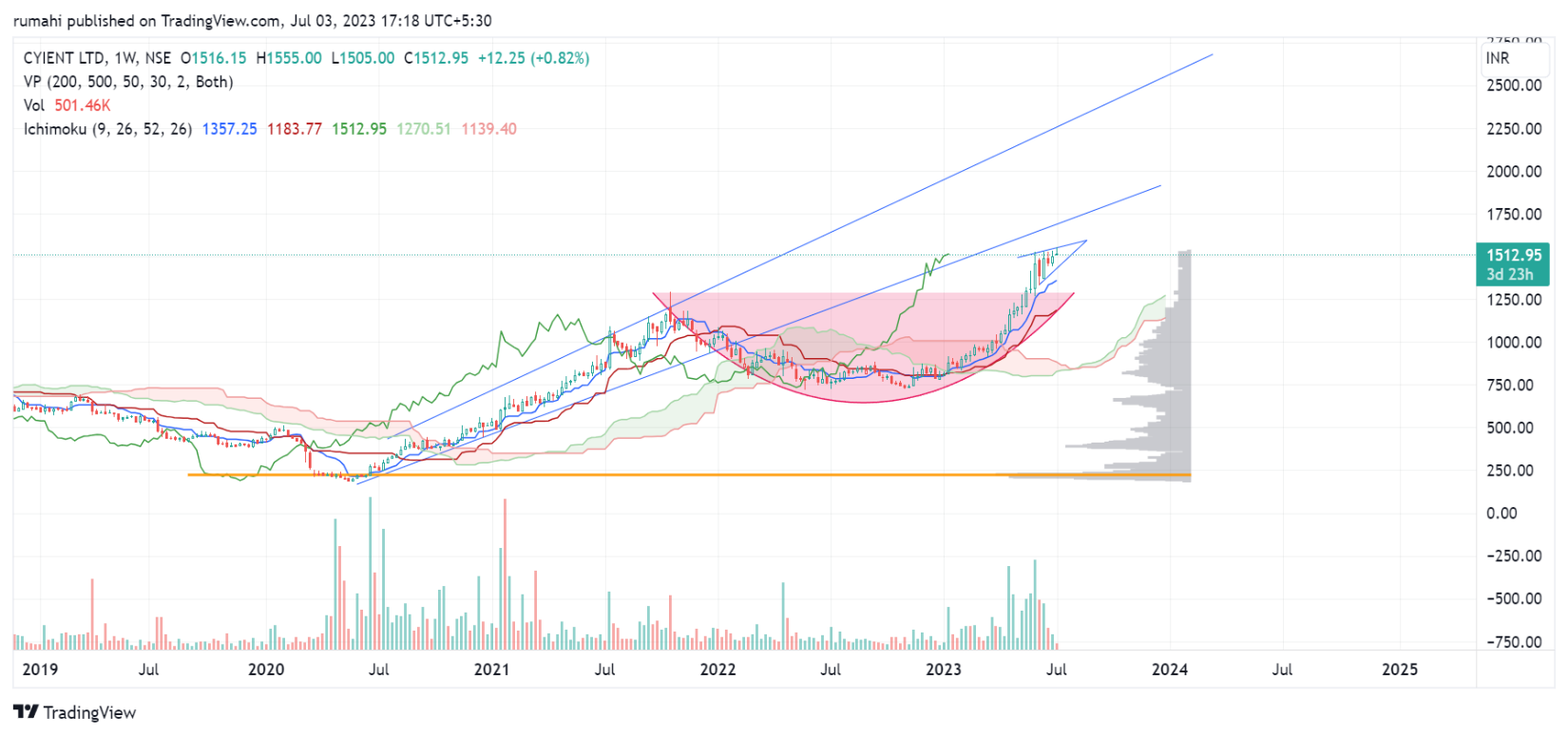

Technical Outlook:

Cyient ltd shown Trend pattern from Levels of 190, towards the levels of 930 on 17-Jan-2022, Stock broken the Levels of 930 on closing basis and re-tested levels of 730 on 31-oct-2022. Stock after long consolidation shown CUP pattern breakout above levels of 1290 on weekly chart on 29-may-2023, and now stock is moving in Triangular pattern with higher high and higher low pattern in range of 1555-1440 Levels any Price Volume breakout above the said Levels will trigger high Levels of Buying Opportunity and we can see Levels of 1680-1730 on immediate Basis, Keeping Strong support near levels of 1400. Stock can touch Levels of 2000-2100 over Long Term. We suggest Buy Cyient ltd and add dips if we get near levels of 1400. Considering the strong demand across its portfolio, along with anticipated margin improvements, we expect the company to maintain its operational performance.

Sustainable demand commentary despite adverse macros:

Aerospace: The Aerospace demand on the MRO and engineering services is relatively strong, while design engineering service is volatile. The design service is expected to gain pace once the development cycle with a new platform gets initiated, although the timeline is uncertain. It expects the vertical to deliver double-digit growth in FY24, in line with the consolidated level growth.

Connectivity: The functional areas on the Telecom Asset and Network Design are ramping up quite well. Both Europe and the US are generating equal opportunities on the network fiberization/throughput on 5G rollout.

Sustainability: It has a larger scope on the regulatory and compliance front. The ancillary services on mining activities using IoT, AI, and sensors are gaining traction among its clients. With the acquisition of Citec, the company now has a significant presence in the Energy, Oil & Gas, and Electrofuel capabilities.

Acquisition of Citec: The company now has a significant presence in the Energy, Oil & Gas, and Electrofuel capabilities. The nature of the work is more on the plant/product engineering v/s plant automation/smart engineering. The enterprises are looking for transitioning to green energy with solutions around sustainability and net-zero emission are gaining traction.

Valuation and outlook:

The company has reduced its dependency on consultants for lead generation and GTM activities and this is one of the key margin levers apart from utilization and SG&A absorption in FY24. CYL’s service segment is shaping up quite well with the majority of its verticals gaining strength. This is majorly attributed to the demand recovery in the Aerospace segment and partly attributed to the inorganic investments. We expect near-term moderation of revenues due to the high base in Q4. However, we expect significant ramp-up in volume in the second half of the year to achieve the service revenue guidance (up 15-20% YoY) in FY24. The valuation is currently trading at 17x and 15x FY24E and FY25E (~40% discount to LTTS), giving us more comfort to assign a higher multiple of 17x (16x earlier) to its FY25E EPS with a target price of INR 1600 with strong support near price of Rs 1410 looking at its forward EPS 67.29 F.Y 2023 and 77.14 for F.Y 2024.