LIC IPO

Date Published: May 3, 2022

Life Insurance Corporation of India (“LIC”) was established on September 1, 1956, under the LIC Act by merging and nationalizing 245 private life insurance companies in India. LIC has been providing life insurance in India for more than 65 years and is the largest life insurer in India, with a 61.6% market share in terms of premiums (or GWP), a 61.4% market share in terms of New Business Premium (or NBP), a 71.8% market share in terms of number of individual policies issued, a 88.8% market share in terms of number of group policies issued for Fiscal 2021, as well as by the number of individual agents, which comprised 55% of all individual agents in India as at December 31, 2021. LIC is the largest asset manager in India as at December 31, 2021 with AUM of ₹40.1 trillion, on a standalone basis which is 1.1 times the entire Indian mutual fund industry’s AUM. LIC has a broad, diversified product portfolio covering various segments across individual products and group products. Their individual products comprise (i) participating insurance products and (ii) non-participating products, which include (a) savings insurance products; (b) term insurance products; (c) health insurance products; (d) annuity and pension products; and (e) unit linked insurance products.

Why is the IPO taking place?

Asia’s third-largest economy was already grappling with a prolonged slowdown even before the start of the coronavirus pandemic. India has recorded its worst recession since independence due to the Covid-19 crisis. Efforts to contain the spread of the virus, such as through stringent lockdowns, created a significant budget deficit and pushed millions into joblessness and poverty. The IPO of LIC will give a boost to the government’s efforts to raise much-needed cash through privatisations, to achieve the benefits of listing the equity shares on the stock exchange & to carry out an offer for sale of 221374920 shares by selling shareholders.

LIC’s Strengths

- Brand value

- Each policy is backed by sovereign guarantee

- Largest agency distribution network comprising upwards of 1.3 cr agents

- Greater % of participation products versus competition, results in relatively higher income or lower loss in initial years for policies underwritten.

Life insurance industry promises great growth potential owing to low life insurance penetration in India vs emerging market countries.

Insurance penetration is calculated as percentage of insurance premium to GDP. The penetration in non-life segment, in fact, slipped to 0.94 per cent from 0.97 per cent in 2018. The life insurance segment recorded higher penetration at 2.82 per cent from 2.74 in 2018. The life insurance segment recorded higher penetration at 2.82 per cent from 2.74 in 2018. In contrast, insurance penetration in Asian countries such as Malaysia, Thailand and China stood at 4.72, 4 .99 and 4.30 per cent, respectively in 2019.

“Globally insurance penetration was 3.35 per cent for the life segment and 3.88 per cent for the non-life segment in 2019. Although the penetration is lower in India for both, it is particularly low for non-life insurance as compared to other countries,” says Economic Survey.

How much of stake will the Government sell?

At present, the government owns 100 per cent stake in LIC. The government is planning to offload around 3.5 per cent of shares. LIC IPO will be entirely offered for sale. The government plans to offer 22.13 million shares of the 6.32 billion shares and no fresh stock will be issued.

You can get India’s biggest LIC IPO allotment only if you have a DEMAT Account. If you don’t already have one, NOW is the time to open yours through StockHolding and cash in on this huge investment opportunity.

Start by opening a FREE* Demat Account through StockHolding. Become eligible to participate in India’s biggest LIC IPO.

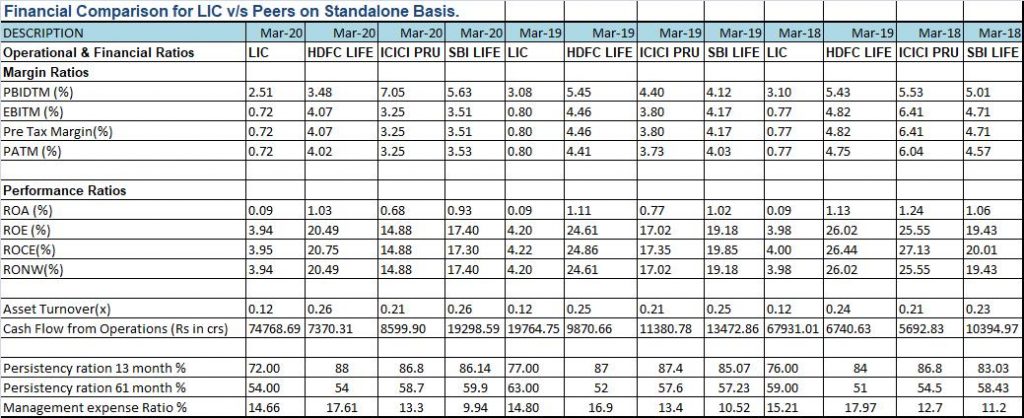

Key Financial for LIC v/s Peer Comparison :

Source : ACE Equities, financial on standalone basis.

QIB Investors: Marquee investors like BlackRock, Abu Dhabi Investment Authority, Singapore’s GIC, Canada’s CPPIB, Fidelity, and Capital International are likely to bid in the QIB segment.

2 MUST Haves, to participate in India’s big LIC IPO

It is mandatory for a policyholder to own a DEMAT Account & and update their pan on the LIC Portal, to Invest in India’s Biggest IPO. According to the DRHP filed by LIC with SEBI, a policyholder who does not update his/her PAN before February 28, 2022 will not be eligible to participate in its IPO. According to the LIC DRPH, “A policyholder of our Corporation shall ensure that his / her PAN details are updated in the policy records of our Corporation at the earliest. A policyholder who has not updated his / her PAN details with our Corporation before expiry of two weeks from the date of the filing of this Draft Red Herring Prospectus with SEBI (i.e., by February 28, 2022) shall not be considered as an eligible policy holder.

LIC’s embedded value stood at Rs.5.4 trillion for September 2021 which is up from Rs.956 billion in March 2021. LIC’s market share in India is unparalleled globally, with no other life insurance player in any other country enjoying such a large market share, LIC said in its DRHP. “

How can an Investor apply?

Investors can apply through multiple choices, multiple categories. He can apply as a Retail investor, as a Policy holder, as an Employee and as and HNI category + Policy holder slab, Retail+ Policy holder category to get a discount as mentioned in the chart. Policyholders can apply as Retail investors (Up to Rs. 2, 00,000 application amount) or HNI (above Rs 2, 00,000). If applying as HNI, they would have to make 2 separate applications as Retail and HNI.

Conclusion:

LIC EV was disclosed in Sep 2021 as 5.4 lac crore. Given govt’s 3.5% stake dilution for the current IPO of Rs 21,000 crore, LIC valuation (as per this IPO price band) = 6 lac crore. Peers of LIC have a market cap ranging from 3 to 6 times EV. LIC is expected to enjoy a market cap / EV multiplier of 1.3 to 1.5, which implies a market cap valuation of 7 to 8.1 lac crore. Hence, there is an upside prospect from both listing gains and long term investment gains perspective.