SBI life insurance Limited – With us, you are sure.

Date Published: November 18, 2022

Company Overview

SBI Life Insurance Co Ltd (SBI Life), a subsidiary of State Bank of India, is an insurance company that offers life insurance products. The company offers individual plans such as unit linked plans, child plans, pension plans, protection plans, and savings plans. It offers group plans which include group employee benefit retirement and protection plans. SBI Life Insurance also provides savings protection products, micro insurance plans, group loan protection products, health plans, and banking product packages including housing loans and personal loans. The company’s services include premium calculator, child education planner, tax calculator, easy plan finder, NRI services, SMS based services and premium payment procedure. SBI Life is headquartered in Mumbai, Maharashtra, India. The company reported revenues of (Rupee) INR829,832.9 million for the fiscal year ended March 2022 (FY2022), an increase of 1.3% over FY2021. In FY2022, the company’s operating margin was 2.1%, compared to an operating margin of 2% in FY2021. In FY2022, the company recorded a net margin of 1.8%, compared to a net margin of 1.8% in FY2021. The company reported revenues of INR48,061.5 million for the first quarter ended June 2022, a decrease of 76.8% over the previous quarter.

Industry Overview

The opening of the sector began in 1990s and last two decades have witnessed a massive transformation of insurance industry in India, both in terms of competition, presence of private players and variety of insurance products. As of the end of FY2021, there were 24 life insurers, 44 general insurers and reinsurers (including specialised insurers, standalone health insurers and foreign reinsurers’ branches) in India. India’s insurance market share is majorly held by the public sector companies, even though their share has been declining over the years. Since the formal inception of insurance sector in India, many major changes have been done by the government and IRDAI for fostering the growth of sector with presence of effective competition. In December 2014, the government approved increasing the FDI limit in the insurance sector from 26% to 49%. In the Union Budget FY2021-22, the government raised the industry’s FDI cap from 49% to 74%. The General Insurance Amendment Bill was padded in August 2021, which aims to push greater private participation in the public sector insurers. The bill seeks to remove the requirement that the Centre should hold not less than 51 per cent of the equity capital in such insurers. India’s insurance industry has registered an impressive growth rate over the last two decades owing to the increasing participation of the private sector. Though the 3 rd wave of COVID-19 with new variants started in January 2022, it had far been less severe than the prior waves. Following the preventive measures of the Government including micro level restrictions, the contact-intensive services are temporarily impacted, industrial activity remains robust supported by government spending and healthy global demand. The GDP growth rate for Q4 FY 2022 stood at 4.1% as compared to 5.4% in Q3, 8.4% in Q2 and 20.1% in Q1 FY 2022. The GDP growth rate for FY 2021-22 stood at 8.7%. This overall growth rate has been a good indicator given the challenges, such as the impact of different variants of COVID-19 as well as the high commodity prices, faced by the economy during the year. Further, according to IMF estimates (April 2022), India’s economy is estimated to grow by 8.2% in FY 2023.

Result Highlights of Q1 FY23:

- Gross Written Premium (GWP) grew by 35.5% YoY to INR 1,13,491 Mn in Q1FY23, mainly driven by 67.2% YoY growth in NBP and 14.4% growth in renewal premium.

- Value of New Business (VNB) grew by 131.6% YoY to INR 8.8 Bn in Q1FY23 with margins at 30.4%.

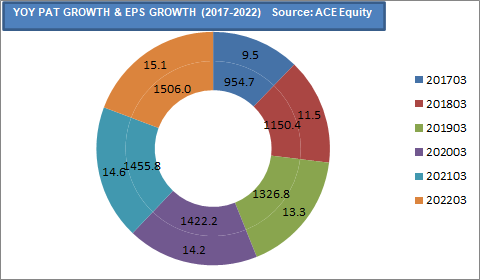

- Profit after Tax (PAT) stood at INR 2,629 Mn in Q1FY23, a growth of 17.8% YoY, while a decline of 60.9% QoQ.

- Bancassurance NBP saw a growth of 94% YoY while agency channel posted a growth of 50% YoY. Thus, share of banca improved from 45% in 1QFY22 to 52% in 1QFY23

- Credit life protection business grew 63% YoY to INR4.1b on NBP basis.

- SBI Life aims to grow premiums by 25%+ on a sustainable basis.

Key Concall Highlights

- SBILIFE has launched SBI Life Smart Annuity Plus, which offers a comprehensive range of ability with an option of deferred annuity payoff.

- SBILIFE has signed up with Paschim Banga Gramin Bank, a leading RRB in West Bengal to broaden its reach.

- It has also signed an agreement with PhonePe Insurance Bookings Services limited to be agile with changing customer behavior.

- Single premium contribution stood 28% of the Individual New business premium, which is mainly attributed to growth in individual annuity product.

- Non-par guaranteed product new business has registered a growth of 621% YoY, owing to the new business increased contribution of Smart Platina Plus. This product was launched in March and has seen a strong traction in the new business premium because of the products featuring. Which is gaining a high acceptance in the market.

- The growth in VNB and VNB margin was on account of new business premium growth owing to higher sales and change in product mix with predominantly non-par guaranteed saving segment growth.

- SBILIFE expects to maintain the healthy growth rate in VNB owing to its growth targets in product mix shift.

- The company continued with an efficient use of technology for simplification of processes with 99% of individual proposals being submitted digitally, 40% of individual proposals are processed through automated underwriting.

- On operational efficiency, OpEx ratio reduced to 6.6% for Q1FY23 to from 7.2% for Q1FY22.

- The total annuity and pension underwritten by the company is INR 11.6 Bn, registering a growth of 7% YoY in Q1FY23

Valuation and view:

SBILIFE displayed a strong show in 1QFY23 with 80% YoY growth in APE along with a sharp jump of 132% YoY in VNB. VNB margin spiked ~665bp YoY fueled by a shift in underlying product mix in favor of high-margin products such as Non-PAR and Protection. Despite volatility in capital markets, ULIPs grew 33% YoY. All distribution channels contributed to the growth along with a rise in productivity of banca and agency channels. This led to a better cost ratio and SBILIFE continues to maintain cost leadership. Persistency improved across all key cohorts. We estimate 27% CAGR in APE over FY22-24. We further estimate VNB margin to remain steady from hereon to reach ~30% in FY24, thus enabling 36% VNB CAGR, while RoEV sustains at ~22%. We retain our BUY rating with a revised TP of INR1,500 (based on 2.6x FY24E EV).