SIEMENS Limited – “Ingenuity for life”

Date Published: November 18, 2022

Company Overview

Siemens Ltd (Siemens India), a subsidiary of Siemens AG, is a provider of technology-enabled solutions. The company’s product portfolio includes building technology, energy, railway signalling equipment, drive technology, financing, healthineers, industrial automation, mobility, software, and consumer products. The company also provides various services such as IoT, real estate, business, and building technology services. Siemens India markets its products and services to various industries such as aerospace, automotive, construction, pharmaceuticals, food, and beverage, marine, mining, oil and gas, power utilities, transportation and logistics, cement, technology and communication, tire, and others. The company has business operations in Asia, Europe, the Middle East, Africa, and North America. Siemens India is headquartered in Mumbai, Maharashtra, India. The company reported revenues of (Rupee) INR136,392 million for the fiscal year ended September 2021 (FY2021), an increase of 37.1% over FY2020. In FY2021, the company’s operating margin was 8.9%, compared to an operating margin of 7.8% in FY2020. In FY2021, the company recorded a net margin of 8%, compared to a net margin of 7.7% in FY2020. The company reported revenues of INR42,583 million for the third quarter ended June 2022, an increase of 12% over the previous quarter.

Industry Overview

Manufacturing is a key contributor to the economic development of any nation. The Capital Goods sector is critical to the manufacturing sector as it provides the much needed machinery and equipment to various manufacturing sectors such as Engineering, Construction, Infrastructure, Consumer goods, amongst others. The Capital Goods industry contributes about 12% to the total manufacturing activity in India which translates to about 2% of GDP. However, this is far lower compared with other countries such as China where the sector contributes 4.1% to its overall economy, 3.4% in Germany, and 2.8% in South Korea. Quite clearly India is less capital intensive than these nations and as the proportion increases will lead to exponential growth with improved Incremental Capital Output Ratio (ICOR). The capital goods market In India is fragmented with majority of operational units in the Small and Medium Enterprise (SME) sector, beyond few large players. These are involved in low-value added fabrication and assembly works and cater to small segments of a sub-sector, often serving domestic demand only. Due to their low scale of operation they are unable to compete effectively with large foreign competitors. The growth of the Capital Goods sector in India has been led by increasing demand. However, the sector is less self-sufficient and depends upon imports to meet its domestic requirements to a large extent. The country meets almost 40% of its demand through imports. In order to reduce dependence on imports and boost domestic manufacturing, the Government of India came up with various measures such as National Manufacturing Plan (2012), Make in India (2014) and National Capital Goods Policy (2016). The National Capital Goods Policy (2016) envisages increasing production capital goods from Rs. 230,000 crore in 2014-15 to Rs. 750,000 crore in 2025. It envisages increasing exports from 27% in 2014-15 to 40% in 2025 of production while increasing share of domestic production in India’s demand from 60% to 80%, thus making India a net exporter of capital goods.

BUSINESS SEGMENTS : Overview and Performance:-

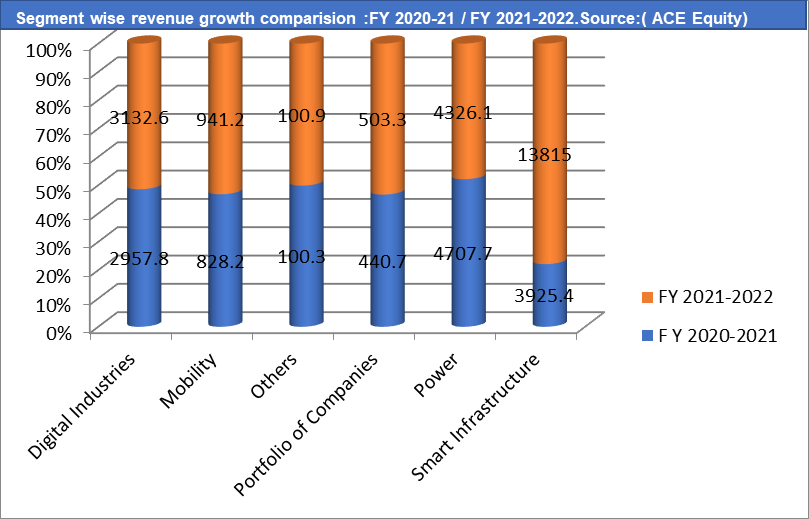

Business : Energy

- Provides integrated solutions, products, and services for oil and gas, independent power producers, utilities, transmission system operators, chemicals, mining, and engineering, procurement, and construction (EPC) companies. Also offers sustainable products, solutions, and services for marking fossil energy greener. Reported revenue of INR47,077 million for FY2021, which grew 16.6% YoY, and recorded negative growth of 4.5% during 2019-21. The segment accounted for 36.3% of the company’s revenue in FY2021.

Smart Infrastructure

- Provides products, solutions, systems, and services for the transmission and distribution of electrical energy for industrial companies, infrastructure segments, and power utilities. Portfolio comprises systems for low and medium-voltage distribution; solutions for smart grids and energy automation; and low-voltage power supply systems. Also offers intelligent and connected infrastructure solutions for buildings and grids.

- Reported revenue of INR39,254 million for FY2021, which grew 50% YoY, and recorded a CAGR of 5.7% during 2019-21. The segment accounted for 30.3% of the company’s revenue in FY2021

Digital Industries

- Offers leading-edge automation, and software technologies for hybrid, process industries, and discrete industries. Portfolio includes industrial software, covering product design, automation, and drive technologies for optimizing the manufacturing value chain, production planning, engineering, execution, and after-sales services.

- Reported revenue of INR29,578 million for FY2021, which grew 56.4% YoY, and recorded a CAGR of 6.1% during 2019-21. The segment accounted for 22.8% of the company’s revenue in FY2021

Portfolio Companies

- Provides process solutions, products and services, and mining and minerals solutions for wind and industry sectors such as minerals, irrigation, oil and gas, mining and cement, metals, marine ports, pulp and paper, renewables, and defence.

- Reported revenue of INR4,407 million for FY2021, which grew 14.7% YoY, and recorded negative growth of 2% during 2019-21. The segment accounted for 3.4% of the company’s revenue in FY2021.

Mobility

- Supplies solutions for freight and passenger transportation, which include rail automation systems, rail vehicles, road traffic technology, rail electrification systems, rolling stock components and systems, and IT solutions.

- Reported revenue of INR8,282 million for FY2021, which decreased 1.9% YoY, and recorded negative growth of 17% during 2019-21. The segment accounted for 6.4% of the company’s revenue in FY2021.

Others

- Includes services to other group companies and lease rentals.

- Reported revenue of INR 1,033 million for FY2021, which grew 7.0% YoY, and recorded negative growth of 6.9% during 2019-21. The segment accounted for 0.8% of the company’s revenue in FY2021.

Geography : Within India

- Reported revenue of INR101,942 million for FY2021, which grew 34.8% YoY, and recorded a CAGR of 2.4% during 2017-21. The segment accounted for 78.6% of the company’s revenue in FY2021.

Outside India

- Reported revenue of INR27,689 million for FY2021, which grew 20.1% YoY, and recorded a CAGR of 6.8% during 2017-21. The segment accounted for 21.4% of the company’s revenue in FY2021

Outlook and valuation:

Siemens Ltd (Siemens India) is a provider of technology-enabled solutions. High liquidity position, support from parent group, and revenue growth are the major strengths of the company, even as geographic concentration remains a cause for concern. Strategic initiatives, acquisition of C&S Electrical, partnerships, and joint venture with TRIL Urban Transport could provide growth opportunities for the company. However, competition, foreign exchange risks, and regulations could affect its operations. We remain positive on SIEMENS from a long-term perspective given its 1) strong and diversified presence across industries, 2)focus on digitization and automation products, 3) product localization, 4) healthy balance sheet and 5) high cash flow. Strong order book and enquiry pipeline makes Siemens attractive and value pick. We keep Buy dips approach on Siemens, As it has Shown strong Earning and price has followed the Earning , we see forward EPS at 37.35 F.Y 23 and 49.29 F.Y 24